Who Do I Contact to Continue Cobra as a Dependent

You've likely heard of COBRA before, though the name doesn't give much away as to what it actually does. Generally, COBRA involves the continuation of benefits coverage after someone is no longer part of the company that had provided those benefits.

And the potential loss of healthcare coverage affects millions of Americans — according to research by the Robert Wood Johnson Foundation, about 59% of people in the United States obtain healthcare coverage from their employers.

This article will break down what exactly COBRA means, who is eligible for it, and how long the coverage lasts.

What is COBRA?

In 1985, Congress passed a bill called the Consolidated Omnibus Budget Reconciliation Act, better known as COBRA.

In the past, if an employee changed jobs or got fired or divorced as a dependent, she was at risk of immediately losing her group benefits. Under COBRA, an employee (and possibly her spouse and dependents) has the option to continue group benefits coverage for a limited amount of time, often at her own cost.

Who is Eligible for COBRA?

COBRA provides a valuable stopgap for people whose life circumstances may have changed unexpectedly, and gives them temporary continued coverage in the interim.

You must meet three basic requirements to be entitled to COBRA:

1. Your group health plan must be covered by COBRA 2. A qualifying event must occur 3. You must be a qualified beneficiary

Wondering what a qualifying event is? A qualifying life event for COBRA coverage varies by who is receiving it: employees, spouses, or dependent children. The Society for Human Resource Management has a great post that details each qualifying life event here.

In general, COBRA covers group health insurance plans with 20 or more employees who work in the private sector or state and local governments. However, there are exceptions, including state-covered legislation that supports coverage with smaller companies with less than 20 employees.

The temporary continuation of group healthcare benefits doesn't only extend to a covered employee. It can also go to her spouse or former spouse or dependent children whose health coverage would otherwise be lost.

You may be eligible for COBRA benefits after the following events:

-

Termination or reduction in hours of covered employee (with exception of gross misconduct) - Divorce or legal separation from covered employee - Death of a covered employee - Covered employee becoming entitled to Medicare - Child's loss of dependent status

How to Create a Benefits Package

Use our guide to simplify creating a benefits package.

How Does Cobra Work?

For active employees, employers usually pay for at least a portion of healthcare coverage. However, COBRA only requires the continuation of benefits coverage. It does not require the employer to cover the cost they would usually pay for active employees.

That means eligible recipients for COBRA coverage who decide to activate it will often have to pay the full cost of their health insurance in addition to a 2% administrative charge.

For those who aren't sure if they want to activate COBRA because of the potentially high cost, there is the option of retroactive coverage. An eligible employee will have up to 60 days after her date of COBRA election to retroactively activate coverage.

According to the Department of Labor, the medical care usually covered by applicable group health insurance plans includes:

-

Physician care - Dental and vision care - Prescription drugs - Inpatient and outpatient hospital care - Surgery and other major medical benefits

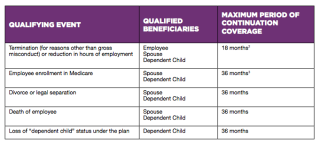

How Long Does COBRA Coverage Last?

The Department of Labor offers this handy chart as shown below. It explains the maximum continuation of coverage after a qualifying event.

So, for example, if an employer no longer covered a dependent child in their group healthcare coverage, an employee would have 36 months of remaining coverage for that child from the same healthcare provider, though likely paid on their own dime.

For a deep dive on COBRA coverage, there are many other provisions to learn about, such as the Health Coverage Tax Credit (HCTC) and how to pay for continued coverage. You can learn more details about particular provisions that will apply to you at dol.gov.

This content is not intended for tax or legal advice.

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, legal or tax advice. If you have any legal or tax questions regarding this content or related issues, then you should consult with your professional legal or tax advisor.

Source: https://www.justworks.com/blog/what-is-cobra-simple-overview-cobra-benefits-coverage

0 Response to "Who Do I Contact to Continue Cobra as a Dependent"

Publicar un comentario